If you’re covered in a group health insurance plan through your employer or your spouse’s employer, should you enroll in Medicare? There are a number of considerations before making that decision.

The first two considerations are very important:

The # of employees at the employer

How you’re eligible for Medicare...based on Age, Disability, or ESRD (kidney failure)

Let’s dive into these two at the same time because they really tie together. And then at the end, we’ll summarize all items to consider when deciding whether Medicare is appropriate for you.

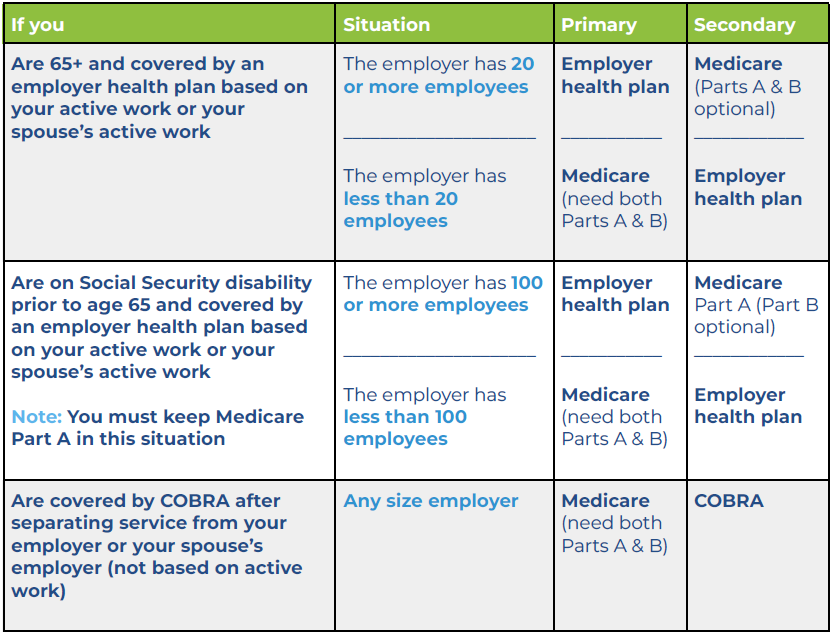

Medicare Based on Age - Turning 65

Large Employer (20+ Employees)

Primary: Group health plan

Secondary: Medicare

You really don’t need Part A or Part B, but some people enroll in Part A because there isn’t a premium. However, enrollment in ANY part of Medicare will prohibit you from contributing to a Health Savings Account (HSA).

DO NOT enroll in Part B in this situation, unless you have End-Stage Kidney Failure. It has a monthly premium and you can delay it without penalty. Reference our Special Enrollment Period instructional page at www.medicaremindset.com/sep

Small Employer (Under 20 Employees)

Primary: Medicare

Secondary: Group health plan

It’s the reverse here. You’ll need BOTH Part A & Part B in this situation as your primary coverage. The group plan will be as secondary coverage. If you don’t get Part B here, your group plan may act like you do have Part B and cover less on outpatient Part B claims.

We always advise to get BOTH Part A & Part B when covered in a small employer plan with less than 20 employees. Some group health plans provide a premium discount for having Medicare as primary. Check with your benefits coordinator to confirm.

Note: Some small employers will join with other employers in an association group health plan. This association setup might allow the employer to be considered a large employer. Confirm this with your plan administrator.

Medicare Based on Disability (Large & Small Employers)

The breakpoint for the number of employees is higher here. It’s 100+ or under 100 employees.

Employer with 100 or more employees...

Primary: Group health plan

Secondary: Medicare

Employer with less than 100 employees...

Primary: Medicare

Secondary: Group health plan

Medicare Based on ESRD - Kidney Failure (Any Size Employer)

If you’re eligible Medicare-eligible (based on kidney failure) and covered in a group health plan (or COBRA continuation coverage)...coordination works like this…

Note: Medicare typically doesn’t start until the 4th month of dialysis treatment. So prior to the 30-month coordination period, only the group health plan is involved. See below…

First 30 months (Coordination Period)...

Primary: Group health plan (or COBRA)

Secondary: Medicare

After Coordination Period…

Primary: Medicare

Secondary: Group health plan (or COBRA)

Medicare & COBRA Continuation Coverage

Primary: Medicare

Secondary: COBRA

COBRA is a continuation of group health insurance coverage after separating service from your employer. It extends 18 months of additional coverage (sometimes up to 36 months). You need BOTH Part A & Part B in this situation.

Before we wrap up with a list of all items to consider, here’s a chart that summarizes what we just talked about:

All Considerations

Here is a list of all items to consider when becoming Medicare-eligible while covered in a group health plan:

# of employees at employer

How you are eligible for Medicare (Age, Disability, ESRD)

Type of health plan you have (PPO, High Deductible Health Plan)

Whether you're contributing to a Health Savings Account (HSA)

How the group plan premium compares to what you would spend while on Medicare and supplemental coverage

Your income (which determines your premiums paid to Medicare)

How the group plan deductible, max out-of-pocket, and other factors compare to Medicare and supplemental coverage

Whether you are a low or high utilizer of medical services

Whether you are also covering a younger spouse or other dependents on your group plan

When you plan to retire

Whether the group plan’s prescription drug benefits are “creditable” or “non-creditable” compared to Medicare Part D minimum standards -- Can be penalized if “non-creditable”

Other -- Whether your employer reimburses you for certain medical expenses, or contributes to your Health Savings Account

Reference Links

www.medicare.gov

Working Past 65 - Medicare & Employer Coverage

Medicare & ESRD (End-Stage Renal Disease)

Medicare & COBRA

Neither Medicare Mindset LLC nor its agents are connected with the Federal Medicare program.