A Medicare Supplement Insurance Plan (or Medigap) can be a helpful addition to your core medical benefits provided through Part A & Part B. If you’re wondering how a Medigap plan works or what it can do for you, you’re not alone.

We’re here to clarify all your questions:

What is a Medicare Supplement (Medigap) Plan?

A Medicare Supplement (Medigap) Plan is a health insurance plan designed to coordinate with Original Medicare (Parts A & B). Medical claims are first filed through Original Medicare and then go to the Medigap plan to do its part. If Medicare approves/allows the service, then the Medigap plan will pay its part as the supplement (based on your plan choice).

What Is Covered By Part A & Part B?

The core coverage provided by Medicare is Part A (hospital) and Part B (medical/outpatient).

In general, Part A covers (allows):

Inpatient hospital care

Skilled nursing facility care

Nursing home care (in certain situations)

Hospice care

Home health services

Part A does not have a monthly premium, as long as the Medicare beneficiary or spouse (who is age 62+) has 40 or more quarters paid into the Medicare system.

Part B covers medically necessary services and preventive services on an outpatient basis. This includes, but is not limited to…

Visits to a primary care doctor or specialist

Medical treatments and tests

Laboratory testing

Durable medical equipment (DME)

Outpatient surgery

Outpatient prescription drugs (in limited situations)

Mental health services

Ambulance services

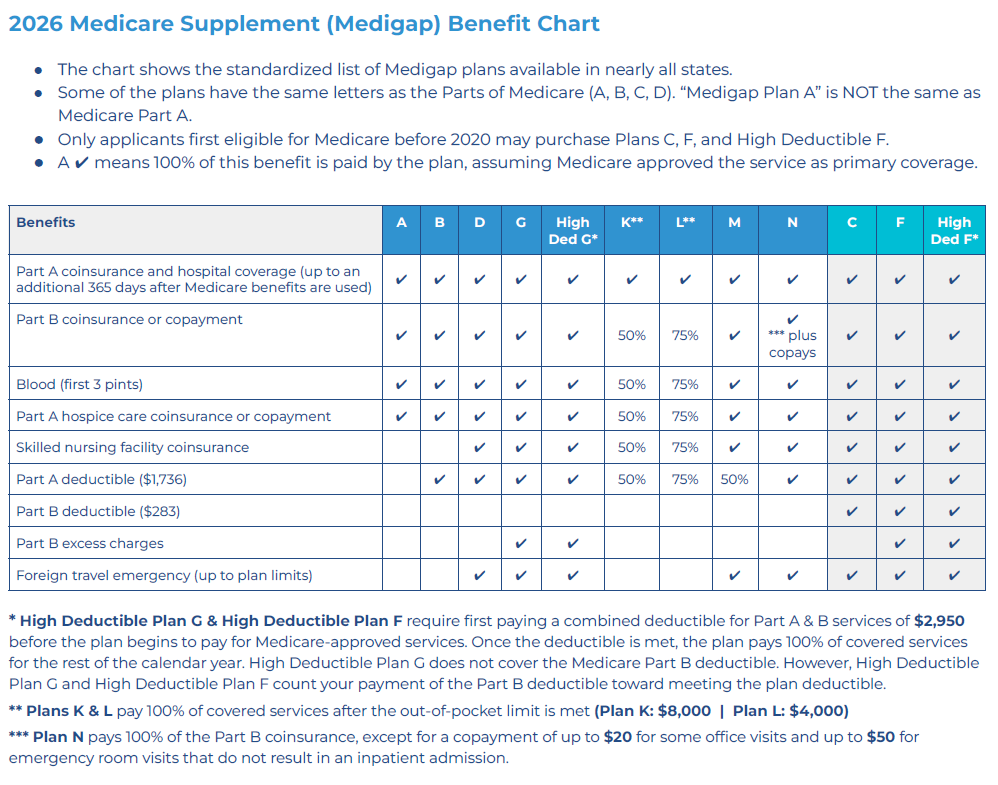

Which Medigap Plans are available to me?

In most states, there is a set list of standardized Medigap plans to choose from. In Massachusetts, Minnesota, and Wisconsin there are different Medigap plans.

Not all plan letters are offered by all insurance carriers, so it’s important to shop around. You can see the standardized list of plans below and how the coverage differs. Some plans can limit your out-of-pocket medical costs significantly, while others require you to chip in more for your medical expenses. But overall, your medical cost exposure is typically less with this setup, compared to an all-in-one Medicare Advantage (Part C) plan.

That’s a lot of letters. Does that mean Medigap Plan A = Medicare Part A?

No. But we understand why that can be confusing. The plans are lettered and use some of the same letters as the “parts” of Medicare (i.e. A, B, C, D), but Medigap Plans A, B, C, and D are not the same as Medicare Parts A, B, C, and D. The good thing, you can rest assured knowing all Medigap plans are standardized, so the same lettered plan has identical benefits across the board (i.e. Plan G with one insurance company has the same medical coverage as Plan G with another insurance company).

When can a Medigap plan be purchased?

Assuming you are at least 65 and enrolled in Medicare Part A & Part B, you can apply for a Medigap plan at any time of the year. However, there are only certain times when a Medicare beneficiary can purchase a Medigap plan without any medical underwriting…meaning your medical history and pre-existing conditions are ignored. Let’s look at three common situations where there’s no medical underwriting:

— “I’m turning 65 and Part B is about to start” — You have a 6-month time frame to get a Medigap plan without underwriting when you turn 65 and your Part B is active. If your Part B is set to begin July 1st, you can get a Medigap plan with these plan start dates (July 1st, August 1st, September 1st, October 1st, November 1st, December 1st, and January 1st).

— “I’m already 65 but delayed Part B to a future date” — Many people work beyond age 65, so they don’t start their Medicare Part B until they absolutely need it. In these instances, such as when you leave a group health plan, you will have access to a Medigap plan without underwriting just as described above. The same 6-month time frame will be provided to obtain a Medigap plan without medical history questions.

— “I’m already enrolled in Part A & Part B, but losing group health coverage” — In these instances, individuals can get a guaranteed issue Medigap plan too, but their options may be more limited. Insurance companies do not have to offer a guaranteed issue Medigap for all of the Medigap plan letters. Some may still offer all of the Medigap plan letters, others might not. It all depends on the insurance company and your state of residence.

Can I switch to a new Medigap Plan?

Yes. You can switch Medigap Plans any time of the year. But if your Part B has been active for more than 6 months, you’ll normally have to answer medical history questions to be considered for approval. Note: Some states have more lenient rules regarding switching plans without medical underwriting.

If you’re application to change plans is denied based on our prior health history, you can stick with your existing plan. Medical history questions can be asked when switching Medigap plans to a different insurance company or even within the same insurance company.

How much does a Medigap plan cost?

Medigap plan premiums can be based on:

—State of Residence: Each state’s department of insurance reviews and approves the premium rates for the insurance companies.

—Zip code/county: Many insurance companies price their plans based on the specific area of the state you reside in.

—Age: If the insurance company uses “issue-age” or “attained-age” rated pricing, the plan premiums are based on your age. This means a 65-year-old will pay less than a 70-year-old for the same plan purchased at the same time. If “community” rated pricing, the plan premiums are designed to be the same for all ages.

—Gender: In general, female rates are less than male rates when comparing the plan offerings at the same insurance company.

—Tobacco use: If you use tobacco, the Medigap Plan premium can be more than a non-tobacco user. This is not normally the case during guaranteed issue situations. Of course, you can expect to see variations from state to state and company to company.

Do Medigap premiums increase over time?

Yes, they can. This should be the expectation from year to year, regardless of where you live and the way the plans are priced. Age, inflation, and other factors can contribute to premium increases over time. But those premium increases are not specific to your medical claims history.

What happens to the Medigap Plan when I move to another state?

Since Medigap plans work in any state, the coverage will not be impacted. You can continue using the plan like normal, but the monthly premium may change in your new residence state. The only action to take is provide the insurance company your updated address. Your premium rate will be updated at that time by the insurance company. Your new premium could be similar, less, or even more than you were paying previously.

Reference Links

When Can I Buy a Medigap Policy?

Switching Medigap Policies

Medicare Advantage (Part C) Plans